Did you know the average landlord in the United States owns 2-3 properties? It’s that first rental property that is the steepest climb. Between stricter lending standards, higher down payments, and unfamiliar qualification hurdles, many would-be landlords delay their entry into the market by years. Yet Blount County's growing rental demand and proximity to the Great Smoky Mountains present compelling reasons to start real estate investing sooner rather than later.

If you're eyeing your first investment property near Maryville, Alcoa, or Townsend, understanding the financing landscape will turn wishful thinking into actual closing dates. Learn what lenders require and which steps you'll need to take before submitting your first loan application.

Why Investment Loans Differ From Primary Residence Mortgages

Lenders view rental properties as riskier than owner-occupied homes. When financial stress hits, borrowers prioritize their housing payments over rental property mortgages. Historical data shows foreclosure rates on investment properties run 30-40% higher than primary residences during economic downturns.

This elevated risk comes out in underwriting. Where a conventional primary residence loan might accept a 620 credit score with 3% down, investment property loan requirements typically start at 680-700 credit scores with 15-25% down payments. Income verification becomes more rigorous, reserve requirements multiply, and interest rates sit 0.5-0.75% higher than comparable owner-occupied mortgages.

Tennessee's investment markets also introduce regional considerations. Blount County's short-term rental boom near the Smokies means lenders here scrutinize seasonal income projections more carefully than they would for traditional long-term rentals. Some underwriters require larger cash reserves to buffer against occupancy gaps.

Typical Loan Types for First-Time Investors

Conventional investment loans dominate the first-time investor space. Fannie Mae and Freddie Mac back these mortgages. Most institutional lenders follow their standardized guidelines. You'll find 15- and 30-year fixed rates, predictable qualification criteria, and the ability to finance up to 10 properties under conventional programs over time.

DSCR (Debt Service Coverage Ratio) loans evaluate properties based on rental income rather than personal income. If the property generates enough monthly rent to cover its own mortgage payment by a specific ratio—typically 1.0 to 1.25—you qualify regardless of your W-2 earnings. Self-employed investors and those with complex tax returns often prefer DSCR products. The trade-offs are higher interest rates and larger down payment requirements than conventional options.

Portfolio and local community bank options deserve attention in smaller markets like Blount County. Regional banks and credit unions hold some loans in-house rather than selling them to Fannie or Freddie, giving them flexibility to customize terms. A Maryville community bank might offer more favorable treatment for a duplex near downtown than a national lender applying cookie-cutter standards. These relationships also matter when you're ready to scale beyond your first property.

Investment Mortgage Guidelines Every Buyer Should Know

Minimum Credit Score Requirements

Most conventional investment loans require minimum credit scores between 680 and 700. Fannie Mae technically allows investment property financing at 620, but lenders add overlays—internal risk policies that exceed government-sponsored enterprise minimums—pushing practical thresholds higher. A 700+ score unlocks better rates and broader lender options.

Lenders demand stronger credit for rental properties because your payment history predicts how you'll handle financial pressure. A higher credit score demonstrates disciplined debt management that persists even when tenants turn problematic or maintenance bills spike unexpectedly.

Debt-to-Income Ratio Targets

Conventional investment loans typically cap debt-to-income (DTI) ratios around 36-45%, though some portfolio lenders stretch to 50% for exceptionally strong borrowers. Your DTI divides monthly debt obligations by gross monthly income. $4,500 in monthly debts against $10,000 monthly income yields a 45% DTI.

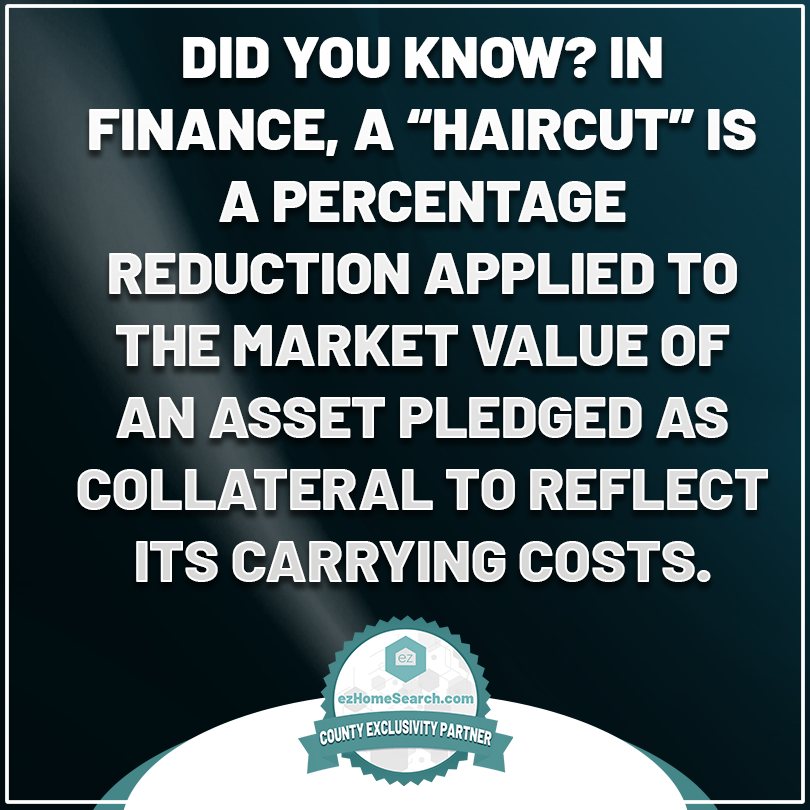

Rental income improves this calculation, but not dollar-for-dollar. Most lenders count 75% of projected rental income toward qualifying income to reflect vacancy rates and maintenance costs. Some programs apply even stricter haircuts for first-time landlords without rental management experience. If you're projecting $1,500 monthly rent, expect lenders to credit you with $1,125 in income calculations at best.

Required Cash Reserves

Investment mortgage guidelines mandate cash reserves equal to several months of the property's mortgage payment. First-time investors typically face 6-12 month reserve requirements. Experienced landlords with multiple properties might satisfy lenders with 3-6 months cash reserves.

These reserves protect you and the lender from vacancy periods, unexpected repairs, or tenant defaults. A $1,200 monthly mortgage payment with a 6-month reserve requirement means you'll need $7,200 sitting in accessible accounts after closing. Retirement accounts can count toward reserves, though lenders may discount their value by 30-40% to account for early withdrawal penalties.

Rental Property Loan Requirements You'll Need to Meet

Down Payment Expectations for Investment Properties

Plan for 15-25% down on your first investment property. Single-family rentals purchased through conventional channels typically require 15-20% down, while multi-unit properties (duplexes, triplexes, fourplexes) jump to 20-25%. These exceed the 3-5% minimum down payments available on some primary residence loan programs.

First-time investors sometimes attempt creative financing to reduce upfront cash, but options narrow quickly. You cannot combine an FHA loan (which allows 3.5% down) with an investment property. The FHA requires owner occupancy. House-hacking strategies where you live in one unit of a duplex while renting the other are the rare exceptions. Terms specify you must occupy the property as your primary residence for at least one year.

Verification of Income and Employment

Lenders want to see two years of consistent income through W-2s, pay stubs, and tax returns. Employment gaps, frequent job changes, or declining earnings patterns raise red flags during underwriting. If you switched industries six months ago or took a pay cut recently, expect additional scrutiny and potentially higher reserve requirements.

Self-employed borrowers face tighter documentation standards. Tennessee's business-friendly environment attracts many entrepreneurs, but mortgage underwriters view self-employment through conservative lenses. You'll need two years of personal and business tax returns, profit-and-loss statements, and sometimes year-to-date financials. The income lenders count equals your average net self-employment income after expenses, a figure usually lower than your gross business revenue.

Property Condition Standards

Investment properties must meet minimum property standards similar to owner-occupied homes. Appraisers flag structural issues, electrical hazards, plumbing problems, and health/safety concerns that could prevent financing. East Tennessee's older housing stock presents specific challenges: outdated electrical panels, galvanized plumbing, aging septic systems, and foundation settling common in pre-1970s homes.

Properties requiring extensive rehabilitation rarely qualify for conventional investment loans. Most lenders want move-in-ready rentals or properties needing only cosmetic updates. If you're eyeing a fixer-upper, you'll likely need alternative financing like a 203(k) renovation loan (which requires owner occupancy) or cash purchase followed by refinancing after repairs.

How to Qualify for an Investment Property Loan as a First-Time Investor

Strengthen Your Credit Profile

Start building your credit foundation 6-12 months before applying. Pay down credit card balances below 30% of available limits. Each monthly statement reporting lower utilization rates incrementally lifts your score. Avoid closing old credit cards even after paying them off. Credit age matters, and closing accounts reduces the total available credit while potentially increasing utilization ratios.

Don't apply for new credit during this preparation period. Each hard inquiry drops your score by 2-5 points temporarily, and recent credit applications suggest financial stress to underwriters. That new car loan or department store card could cost you a better interest rate or even loan approval.

Boost Your Savings for Down Payment + Reserves

Accumulating both down payment and reserves demands discipline. A $200,000 investment property with 20% down plus 6-month reserves requires approximately $47,000 cash at closing ($40,000 down payment + $7,000 reserves, plus closing costs). Start automating transfers to dedicated savings accounts months or years ahead of your target purchase date.

First-time investors sometimes tap retirement accounts for down payments, but proceed carefully. While IRS rules allow penalty-free 401(k) loans and first-time homebuyer IRA withdrawals up to $10,000, these strategies deplete your long-term savings and won't help if lenders discount retirement account balances for reserve calculations.

Show a Strong Financial Picture

Lenders examine 2-3 months of bank statements for both down payment sourcing and reserve verification. Large deposits require explanation letters and documentation. That $15,000 gift from your parents needs a gift letter confirming the funds don't require repayment. Selling a vehicle or receiving a work bonus? Save the documentation proving legitimate origins.

Clean up irregular banking activity before applying. Overdrafts, returned checks, and negative balances suggest financial mismanagement that spooks underwriters. Even legitimate business owners who run personal and business finances through the same accounts should separate these transactions well ahead of mortgage applications.

Getting Pre-Approved With a Blount County Lender

Local lenders who regularly finance Blount County investment properties understand market-specific nuances that national lenders miss. A Maryville-based mortgage broker recognizes that Townsend cabins command premium short-term rental rates during fall foliage season but experience deep winter lulls. This knowledge shapes realistic income projections and appropriate reserve requirements.

Pre-approval reveals exactly where you stand financially. You'll learn your maximum purchase price, required down payment, interest rate range, and monthly payment estimates. This information prevents wasted time touring $300,000 properties when you qualify for $225,000, or worse: writing offers on properties you cannot actually finance.

Investment Property Trends in Blount County

Why Investors Target Blount County

Blount County sits at the intersection of multiple favorable investment dynamics. Knoxville's expanding metro area pushes housing demand southward into Maryville and Alcoa, where median home prices remain 15-20% below Knox County equivalents. Commuters accept the 20-30 minute drive for better value, creating steady long-term rental demand.

Simultaneously, the county's eastern border touches Great Smoky Mountains National Park—America's most-visited national park with 14 million annual visitors. Townsend's "peaceful side of the Smokies" branding attracts tourists seeking alternatives to Gatlinburg's congestion, fueling short-term rental growth. Properties within 15 minutes of park entrances command $150-250+ nightly rates during peak seasons.

This dual demand of long-term renters in western Blount County and short-term vacationers near the Smokies gives investors portfolio diversification within a single market. You might hold a Maryville duplex generating $2,200 monthly from two year-round tenants while operating a Townsend cabin producing $4,500 monthly from weekend bookings.

Documentation & Pre-Approval Checklist

Gather these materials before scheduling lender meetings:

Personal financial documents:

Two years of personal tax returns with all schedules

Two years of W-2s or 1099s

Recent pay stubs covering the last 30-60 days

Bank statements for all accounts (2-3 months)

Retirement account statements

Documentation of other assets (stocks, bonds, life insurance cash value)

Business documents (if self-employed):

Two years of business tax returns

Year-to-date profit-and-loss statement

Business bank account statements (2-3 months)

CPA letter verifying continued business operation

Property information:

Target property address and listing details

Estimated monthly rental income with comparable rent data

HOA documents if applicable

Preliminary title work or property deed

Credit items:

List of monthly debt obligations with balances and payments

Explanation letters for credit inquiries or derogatory marks

Payment history documentation for non-traditional credit (rent, utilities)

This documentation accelerates underwriting and prevents delays caused by missing paperwork. Lenders typically issue pre-approval letters within 24-48 hours once they've reviewed complete documentation packages.

Working With a Local Real Estate Agent Who Understands Investor Needs

The right real estate agent amplifies your success as a first-time investor. Experienced investment property agents evaluate deals through cash flow lenses rather than emotional appeal. They calculate cap rates, identify value-add opportunities, and flag properties with financing complications before you waste time on unworkable deals.

General residential agents might miss Blount County’s unique investment-related regulations. Zoning restrictions limit short-term rentals in some neighborhoods while other areas welcome them. Septic system capacity determines whether you can convert a three-bedroom home into a four-bedroom rental. County flood maps affect insurance costs and financing availability along Little River and other waterways.

Investment-focused agents also maintain lender relationships that smooth your qualification process.

They know which local mortgage brokers specialize in rental property financing, which appraisers understand investment property valuations, and which title companies move efficiently through investor transactions. These connections compress timelines and reduce friction throughout closing.

Your Next Steps Toward Investment Property Ownership

Qualifying for your first investment property loan in Blount County requires more preparation than buying a primary residence. However, the barriers are entirely surmountable for disciplined savers with decent credit. Start building your financial foundation now.

Connect with a local lender early in your process, ideally 6-12 months before you plan to purchase. This timeline allows you to learn about the market and adjust to approaching real estate as an investor. With their insight, you can adjust your savings targets based on real numbers rather than estimates, and position yourself to act quickly when the right property appears.

About the Author: Preston Guyton is the founder of ez Home Search. He has been a real estate leader for over 20 years. Starting with a focus in South Carolina, he has helped coach and empower real estate professionals to achieve their full potential by meeting the needs of their local community.